The Market During Wartime

Recently, the U.S. began strikes against Iran. This type of action can cause worry and fear across many facets of our lives. One of these is the market. What will this mean for my investment portfolio? What should we do?

It is common for a temporary pullback in the market to follow this type of action. We have seen this many times. For example, when Russia invaded Ukraine in 2022, we saw the S&P 500 drop about 7% within about 17 days, taking 27 days to recover. This also includes the impact on crude oil prices. In 2025 when the 12-Day War occurred, the S&P 500 dropped over 1% in 5 days, taking 7 days to recover. Whew. That wasn’t too damaging. During larger conflicts though, such as the Iraq invasion of Kuwait in 1990 where they seized the oilfields, the S&P 500 plummeted almost 16% in 50 days, the recovery of which was quite longer at 4 months, followed by another drop as we prepared for Desert Storm.

The recent war with Iraq is no different. And neither is our investment strategy.

But isn’t there an alternative? High Yield savings accounts are still offering good rates. As of today, marcus.com is paying 3.65%. Sounds pretty good, right? Definitely worth it to store short-term money you expect to use in the next couple years.

But when it comes to retirement, when money is expected to grow and keep pace with inflation for a long duration of time, this can be risky as well. Not in terms of losses, but in purchasing power. For example, the national average for a gallon of gas 10 years ago was $2.14. Today, the national average is $4.02. This means the cost of gas inflated by an average of 6.5% a year. Your money would not have been able to keep up with this growth if invested “safely” in a high yield savings account, even assuming you had this great interest rate the entire time. Long term, you need more growth than that.

What if you can time the market? Oh, how much easier life would be if the market was predictable. Long-term, we can predict growth. But to beat the market, we need to know what the market might do in the short-term. I believe doing that consistently is impossible.

My clients have probably heard the phrase “stay in our seat” more times than I can count. This originated from a lecture I heard when I was just a baby financial planner. The speaker spoke of a hockey game he had recently attended. The game was pretty boring, with neither team scoring a goal for quite some time. Finally, he decided to grab a drink and headed to the concourse. The line was long, but he slowly made his way toward the front. Suddenly, he heard the horns and the crowd erupted. His team had scored a goal and he had missed it. He briefly considered abandoning the line to head back, but he was so close to the front. What were the chances they’d score again so quickly? As he finally made it to the counter, he heard it again. He’d missed the second goal. He hurried to his seat, but no other goals were scored that game.

The market moves just like this. When rebounds come, they are often sudden. And if you aren’t in your seat, you miss them. Hence the phrase, stay in your seat. (This analogy has become all too real, as I find myself marrying a bonafide hockey fan in the next couple months and I have seen a lot of hockey games. Go Sharks!)

The good news is, we don’t have to predict the market correctly (twice - when to sell and when to buy back) to have a positive investment experience. All we need to do is choose an allocation we can live with, even during those tense times, and stay invested. Sometimes this is harder than it sounds. I was a new planner during the bear market of 2008-2009, but I learned so much during that time and saw first-hand the damage that happens when we let our emotions dictate our actions. Fortunately, your planner has ways to make these times a bit more comfortable.

If this sounds like a broken record you’ve heard a hundred times before, good. We are doing our job. When we take on clients, we give them a nice strong vaccine to inoculate us from the emotions around investing and when we meet and we tell you the same repetitive stories, examples and metaphors, we are simply giving you a booster shot.

“Oh my gosh, Michelle! This is so boring! Give me something ground-breaking I can use!” Well, smart investing can be relatively boring. That’s not to say we aren’t continually looking for educationally backed ways to make your Portfolio better. Our investment committee meets regularly to ensure we are making the best decisions possible when building portfolios. Whether it is to alter the divide between international and domestic stocks to more closely match the world investment map or leaning towards exchange-traded funds rather than mutual funds for their tax-advantaged treatment, we recognize some things evolve over time and we can too. The fundamentals though? They stay the same.

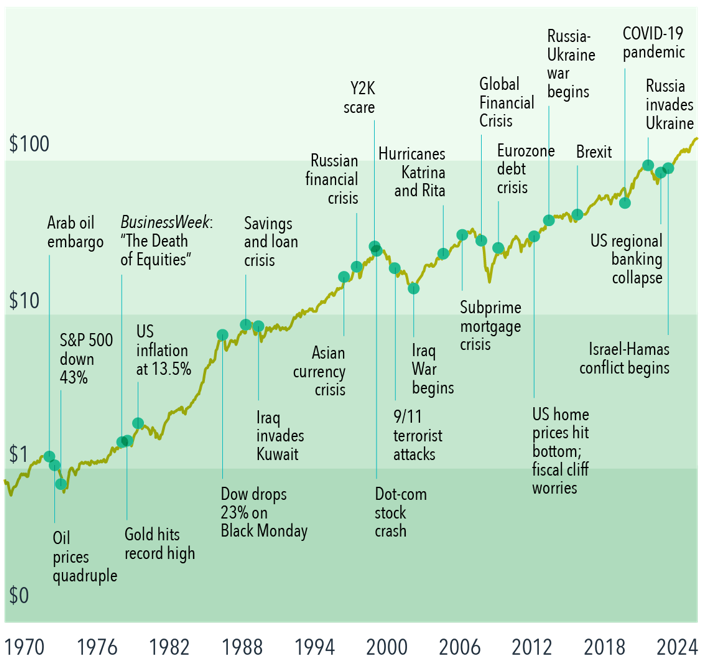

When we reach a new high? Awesome! We are always doing that. When the market drops? Yep, that’s to be expected. Does war mean a bear market is coming? Sometimes. But we are ready for that. I included a chart below that shows previous conflicts and the market’s reaction. Is there a pattern? Yes. The pattern is eventually we reach another new high.

The flavor varies but the product doesn’t change. Our portfolios hold ownership in thousands and thousands of companies across a dozen asset classes. Whether the next crisis is war or economic decline or a change in political leadership, we are prepared to for the (sometimes) wild ride to the next new high.

If you find yourself struggling with market worries, reach out to your planner. I consider helping clients through tough times one of my greatest privileges (and responsibilities). War can be devastating for many reasons, but permanent damage to your portfolio shouldn’t be one of them.

*Chart from Dimensional Fund Advisors

Michelle Carter, CFP®

Find Michelle on Linkedin